The Covid Market

Wear a Mask....Stonks Go Up....BRRR.

Since this stock market is a bit of a circus, I figured I’d offer some observations here versus outright investing ideas.

Some observations…..

Stock volatility is very high.

Yea, it’s a very sky is blue thing to say, but it’s actually very relevant in this market. Where the VIX is at today basically implies 2% daily moves for the S&P 500. Individual stock volatility is a lot higher. We spent the better part of last 12 years with virtually no daily volatility like this. A couple brief spurts here and there, but nothing like this.

What does this mean in layman’s terms?

It means notable stocks can move 7-10% for no reason whatsoever on any given day. It’s what takes Zoom up 40% in a day to only give it back a in a week, and then notch a new high 2 weeks later. Yes, there are attempts to ‘explain’ moves with analyst news/announcements/covid elements/election/stimulus etc because that is human nature. The stock market is not supposed to be a complete total casino, and you can still rationalize away whatever it is you want with some degree of future discounted outlook. However, for those of us who have lived through 20+ years of tape that current price action/news flow nexus is least reliable it’s ever been.

And there is a very good reason for that……

There Are A lot of Newbies in The Market

While most investing bubble talk is often spent focusing on valuation, the reality is all bubbles tend to be about human behavior. Meaning you can’t really call something an asset bubble till people start speculating in very raw fashion. It’s one of those you know it when you see it type things. But when it’s all over with, the cautionary tales of stock speculation almost always revolve around the day traders. Whether in a back alley street in London, in some desert garage in Kuwait, in a boiler type room OTC operation, at a day trading electronic firm in the suburbs, online in a home office, or on some mobile App; the day-trader is always found guilty as charged at the end of a bubble.

-The internet bubble is often associated with day traders and the beginning of online trading.

-Mrs. Watanbe ruled forex trading between cooking meals during the Japanese Carry trade.

-The GCC had a similar phenomena in 2005-2006

-China’s stock bubble in 2015 was remembered for its army of day traders.

-Millenial Robinhood day traders and the likes of DDTG have been front and center under Crypto and now Covid.

Anecdotal stories on retail speculation get highlighted here and there in the midst of a bull market, but they really don’t draw too much attention until a bull market has clearly gone bust. This is because there usually is an underlying fundamental driver to focus on a narrative wise which initially supersedes the animal spirits.

This time is DIFFERENT.

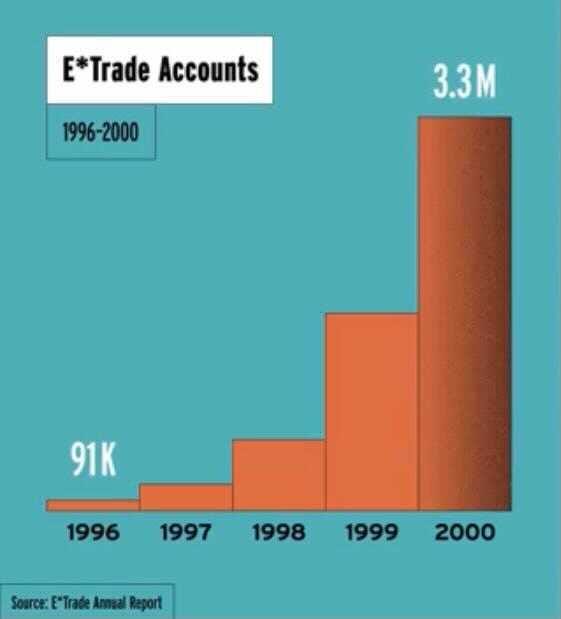

The Covid market is actually quite unique in that day trading has exploded globally as both a means to make money but also as a genuine recreational activity during the lockdown. BarStool’s David Portnoy, for example, was forced into equities because of the live sports shut downs. He was not alone. Many people opened brokerage accounts with stimulus checks as a means to make a little extra income as commissions are zero and they couldn’t return to work.

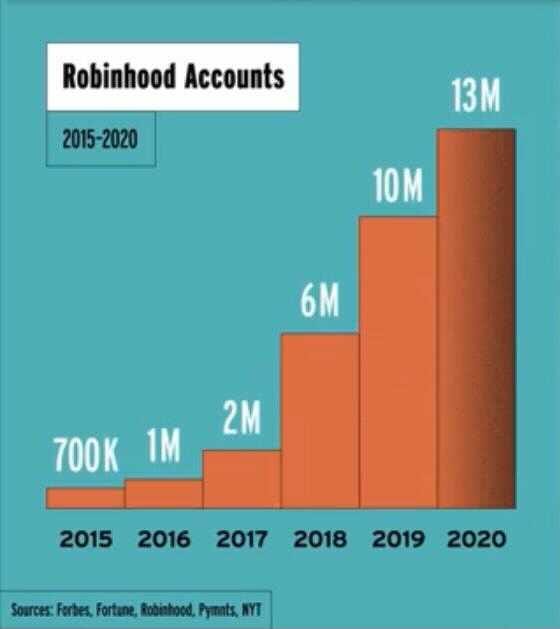

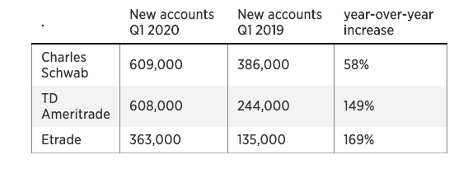

So, while Robinhood may have grabbed the headlines with the new account openings it recorded in the early days; every US broker has seen a boom in account openings. To put it bluntly, the US stock market has acquired more retail traders in a faster period of time than any other time in history.

Now usually this data in of itself would be enough to sound a lot of caution, but the chaos that is Covid has overshadowed this. Which I find interesting because it is in fact the tip of the iceberg……

Robinhood which told us they added 3ml accounts through May to hit 13million in June disclosed that they passed every legacy broker in daily avg revenue trades (DARTS).

Robin hood’s median trader is 31yrs old and over half of them are on their 1st brokerage account. I’m going to guess they are somewhere in 16ml range based on other broker Q2 disclosures.

Now, Americans signing up to trade US equities in record numbers is a story in of itself, but try the whole world doing it at the same time.

Europeans and Japanese retail are just as likely to be trading Tesla as they are listed names in their own markets. But so are Indians with Robinhood like apps allowing millions of new traders to access the US market in manners long thought restricted to only high net worth individuals. Robinhood API’s as a service companies like Drivewealth & Alpaca are making this very easy.

Then there is Russia. I was chatting with institutional sales trader in the Russian market the other day who was filling me in on the appetite for US equities. They have 6ml new accounts on MOEX in last 18mths. Covid+low rates= stock trading in Russia too. Also, Bloomberg recently did a piece on Freedom Holding Corp, a Nevada incorporated brokerage whose main operations are based in Almaty, Kazakhstan. It’s a good read. Here you have a firm that used to rely on 20 day traders for most of its volume which now has 150k+ clients chasing US ipo’s and hot tech stocks.

The Chinese are also back at it again with 2.4ml new brokerage accounts opened in July, and margin trading expansion rate exceeding the 2015 bubble.

Anyway, you get my point. I could probably share five solid Money Game worthy short stories on Covid trading mania across the globe from my own encounters since May. I’ll leave them for another day, but let’s not forget the simple FACT that this is the most “Kids Market” there has been in equities in the modern era. Meaning there is a huge influx of traders who have never seen stocks decline over an extended period of time and who have return expectations that are being validated by the market in real-time which they have little perspective on.

Trading dynamic changes like this are rare occurrences. For example, Robinhood doesn’t offer short-selling. So, every Robinhood trader gets to go straight to options trading if they want to bet on a stock falling. One does have to remember that price is highly sensitive to the marginal trader, and these days that means you need to factor in how an army of traders who have essentially never traded before will behave when you are fundamentally ‘investing’.

Also, at a ripe median age of 31, the Robinhood trader is fearless and so far as he or she is concerned infallible. You cannot rationally explain to them that by simply collectively joining the market at the same time with the same immediate speculative expectations they are in fact sowing the seeds of their very own destruction. Why do I say that? Well, anyone whose been in their shoes can answer that question. And their confidence is contagious to the point even those of us who know better are susceptible to it. Again, this is just an observation, but it’s a hell of a lot more relevant driver of stock price action than anything else these days.

Covid Economics Are Complicated

Home sales and car sales are pretty important things economically speaking, and well we tend to collect a lot of data here. Covid has been wild.

New car production shut down in March for roughly 60 days. So, through July automotive production in North America dropped from 9.6ml to 6.6ml.

Combine this with Covid dynamics that initially favored avoiding Mass Transit and Ride Sharing, and you end up with an automobile shortage in America.

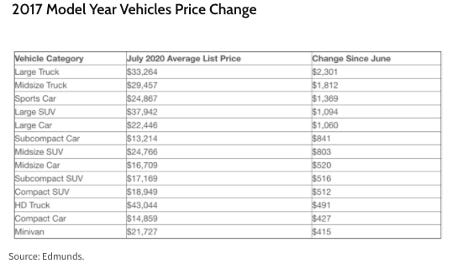

So, used cars just like old baseball cards are hot! Ok, not exactly like baseball card as boredom is not the same Covid problem, but you get my drift. According to Edmunds, US avg car trade in value rose from $12k to $14k in July. To be clear you don’t need to look that up as it’s never happened before.

Then there is housing which is having a good year…..

Existing home sales have been strong as well….

Supply is naturally getting very tight…..

Then there is the other side of the real estate story…..

Covid carnage on the commercial side is not exactly a shocker. Talking to a friend in credit the other day cmbs benchmark though down from its wide March spread is still trading at more than double pre-covid levels. The Colony Capital headline obviously jumps out as Tom Barrack has close ties to Trump, and they essentially offloaded that entire hotel portfolio for nominal cash consideration. So, close relations with the President haven’t helped save over leveraged Hoteliers from Covid. Even Monty Bennett had to return his PPP funds after coming under scrutiny and Ashford Realty Trust stock doesn’t seem to be getting a bump from his China focused article that made waves in March.

Anyway, going back to the start of this observation, the Covid economy is complicated. There are supply shortages for new homes and used cars. There are interest forbearances. There are commercial foreclosures moratoriums. Residential foreclosure backlogs just starting to be addressed. You have tenants not paying rent. Hotels in Times Square closing down. Rural rentals surging. And this is all going to have to rebalance again as Covid subsides.

What will the new equilibrium look like?

That’s a good question, and for the most part the ultimate unknown right now. But in some basic areas you can guess…..

For example, Smart phone sales and notebook sales are likely going to flip directions sometime in the near future. People being less mobile has hit smartphone shipments while demand from WFH and education has caused notable expansion in the notebook market.

Notebooks are hot right now…

You can also start making mid to late 2021 predictions on e-commerce growth, OTT streaming, social media engagement, overall compute infra needs etc as far as Covid comps. Capacity expansion and sudden rapid investment don’t go well with relative demand declines. Again, I am simply trying to focus on making observations here but Shopify for example is doing black Friday levels of traffic daily. They have invested in their infrastructure to meet that new sustained level of demand. However, even if the current Covid pace can be maintained you will see the second derivative affects pretty clearly start to materialize, but what if the ‘covid losers’ economy takes back some share even temporarily next Summer for example?

Will that be disruptive?

I ask these questions because they lead in nicely to my next observation which is that while the Covid economy is complicated; the Covid market narrative isn’t.

Covid Stock Investing Is Simple

Rates are low and liquidity is abundant because Covid created an economic disruption the likes of which the US has not experienced since WWII. Thus, equities are more attractive than ever before for yield seeking investors. Rates will remain low because of Covid and consequently overall economic growth is disappointing. Thus, growth equities will see/experience meaningful multiple expansion. Several notable investors have pushed this narrative. Venture capitalists naturally like it a lot as well as Covid ‘accelerates’ the success of disruptive businesses which in turn means each dollar of revenue their portfolio companies generate is worth multiples of what it was pre-covid. This narrative has helped fuel an explosion of IPOs and SPAC’s.

Consequently, the market mood has evolved from fear and panic to awe with respect to how companies like Zoom, Peloton, Amazon, Walmart, Wayfair, and countless others have prospered from Covid. This euphoria has also recently spread to the extent that strong businesses which are performing very well in this environment, though nowhere near the level of the knee jerk covid winners, are now also viewed w similar awe. Like Nike last week….

This headline doesn’t read Nike revenues down 1% yr/yr as stock surges 50% in same time period. I’ve even seen some arguments attributing the e-commerce growth to the fact Nike’s CEO used to run ServiceNow despite the fact that he’s been there for less than a year. But then again Servicenow is the magic resume right now with their other former CEO, SaaS Rockstar Frank Slootman getting 10x Snowflake market credit after just about 1 yr on the job.

Anyway, euphoria is fine and dandy when stocks move like this, but it’s pretty impressive how all the macro madness that is still out there has almost magically disappeared over the past 3 months.

Nobody is talking stimulus hangovers. Ok not exactly nobody. I did come across this fantastic Amazon seller’s Twitter feed.

Selling Dog Cages under Covid is $$$! If he could Spac this biz he’d get 15x easy for it here. But unlike S&P 500 management conference calls this seller is already signaling he expects a Covid Cliff despite being 10x yr/yr on the bottom line, so Spac promoters will be steering clear.

Consequently, I am not surprised that there is nobody out there arguing that low rates may ultimately translate into depressed multiples as growth disappoints and govt stimulus crowds out productive investment. Even the money printing narrative as a driver for the stock market isn’t as focused on as it was early on. You don’t see the ‘haters’ who felt stocks shouldn’t go up in a crisis or that bankrupt stocks shouldn’t be surging. In fact, you could argue removing the Robinhood actives list has helped convince at least a few people that this market is perfectly normal. Again this is just an observation. Don’t read this as some hint to ‘short stocks’ cause it ain’t. I’m just pointing out that day-to-day I see a lot fewer skeptics than few months ago and a lot less interest in the macro. And that this is how you get financial headlines that often are surface confusing.

I could go on and on here with respect to this but as i’m podcasting, tweeting, and now Substacking I think I’ll let that all speak for itself.

Really nice write-up!

Just wanted to highlight that there are some people expressing concerns that the current high valuations mean that the 20s could be a lost decade for equity returns. Here is Blackstone CFO Michael Chae:

“I think you can have disappointing long term earnings growth with multiples coming in a little bit, and I can see anemic equity returns over the next five to 10 years…I think this could be a lost decade in terms of equity appreciation”

Link: https://theweeklytranscript.com/2020/09/21/the-transcript-09-21/#content:~:text=The%2020s%20could%20be%20a%20lost,%E2%80%93%20Blackstone%20(BX)%20CFO%20Michael%20Chae